Health insurers pay you to wear smartwatches: 7 programs

Founder & CEO, Smartlet - CentraleSupelec engineer - Concours Lepine 2025, Awarded - CES 2026

Table of contents

Key takeaways

| Point | Details |

|---|---|

| Incentives drive adoption | Insurers translate wearable use into premium discounts and cash rewards that encourage ongoing device adoption |

| Dual wear solves the collector dilemma | Smartlet lets you wear both a mechanical watch and a smartwatch on one wrist without sacrificing sensor accuracy or style |

| Wearable data reduces insurer costs | Longitudinal activity data supports prevention and lowers chronic disease risk, cutting healthcare spending for both parties |

| Personalized premiums ahead | The industry is moving toward real-time premium adjustments based on individual wearable data rather than generic risk pools |

John Hancock gives you an Apple Watch for $25 and cuts your premium by 25% if you wear it. UnitedHealth pays up to $1,000 per year for wearable data. Vitality operates in 41 markets serving 42 million people. Insurers have decided the smartwatch belongs on your wrist - and collectors leaving theirs on the charger are leaving money on the table.

The repairs are being paid for. The ethical problem exists. So, what options are there for the watch enthusiast who would like to continue wearing their mechanical watches?

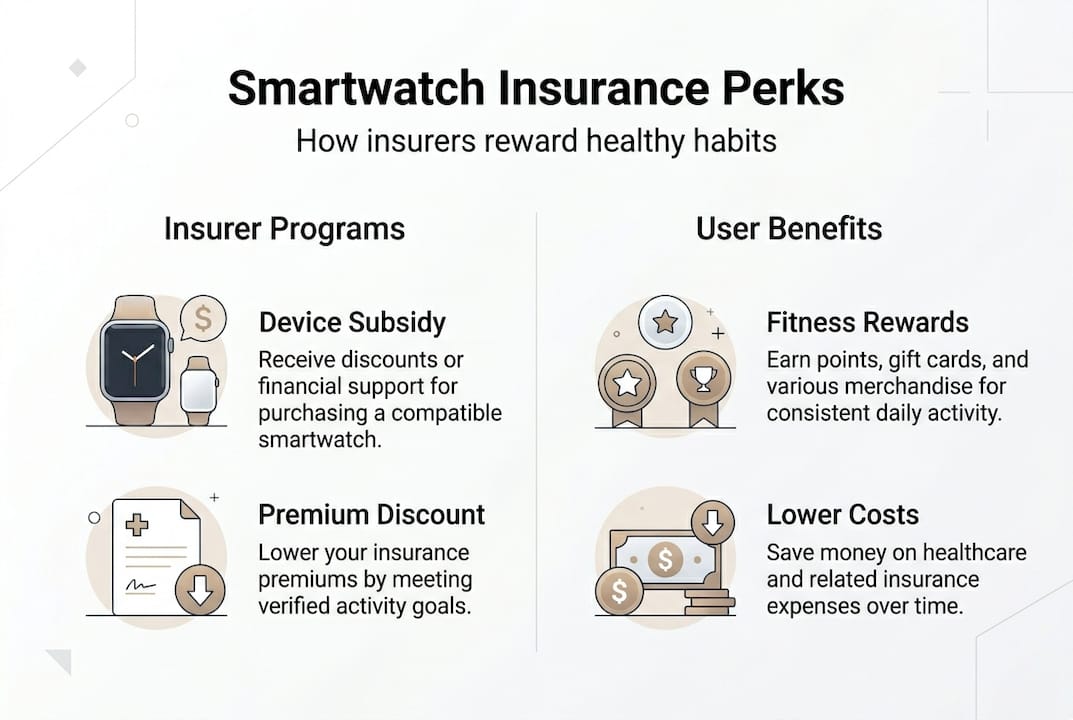

How health insurers incentivize smartwatch use

A few large insurers have taken wearables from a niche curiosity to a coverage that can make good financial sense and perhaps nudge people to change their behaviors. The prices of the new insurance rewards are structured with the actuarial goal of encouraging people to adhere to a fitness wearables regimen that can yield real health behavior change at the population level.

John Hancock Vitality offers an Apple Watch for $25 upfront with activity-based rewards distributed over 24 months. Members who hit daily activity goals earn premium discounts scaling up to 25% on annual life insurance premiums. Apple Watch members earn 7x more Vitality points than non-wearers, and 92% wear their device every day.

Save up to 25% on Apple Watches through Vitality UK's rewards programme. Members can earn points by logging workouts, attending health screens and preventative care health checks. Members can claim an Apple Watch on credit with Vitality, and earn points that reduce and even pay off the monthly credit repayments, so that the Apple Watch is free for members to use, as a result of their healthy behaviour.

UnitedHealthcare UHC Rewards Program Rewards up to $1,000 annually in the form of incentives for connecting fitness trackers and wearables to tracking apps, as well as for completing a health risk assessment and participating in other wellness activities. UHC Rewards offers two types of incentives to members for engaging in healthy behaviors. Members earn credits for working out, achieving certain biometric measurements and for answering health and wellness related questions. The credits can then be redeemed for a cash payout, a merchandise gift card or a discount on monthly premiums.

Eligible devices span the major platforms:

- Apple Watch Series 0 through Ultra 3

- Fitbit Charge 5/6, Sense, and Versa series

- Garmin Fenix, Forerunner, and Venu lines

- Samsung Galaxy Watch series

- Google Pixel Watch

Collects data such as steps, active minutes, heart rate, sleep quality and intensity of workouts. The insurer uses secure APIs to link up with the wearable devices and turn the wearer's biometric data into dollars and cents in terms of rewards and discounts. Of course, this is not ideal for the many watch collectors out there that also need to wear a "smartwatch" to take advantage of the possible savings.wear a smartwatch safely alongside a luxury watch, the financial upside justifies solving the wrist real estate problem.

Both programs share the same architecture: a base reward for participation, variable bonuses for hitting goals, and integration with broader wellness ecosystems. The Smartlet modular strap adapter ensures you never miss a step count or heart rate reading while wearing your Rolex Submariner or Omega Speedmaster.

John Hancock Vitality members who consistently meet activity goals see measurable premium reductions that compound annually - turning daily movement into long-term savings. The collector who also wears a mechanical watch loses nothing with Smartlet.

The actuarial science behind wearables and cost savings

Major insurers are investing in wearable health technology because the data works as an early warning system for conditions that are far cheaper to treat when caught early. Actuaries focus on the long-term data showing that wearable sensor tracking leads to more active people, fewer chronic illnesses, and lower healthcare claims.

Exercise reduces chronic disease risk more cost-effectively than medication. Research comparing wearable-driven lifestyle changes to metformin therapy found a 58% reduction in type 2 diabetes onset versus 31% for pharmaceutical intervention. The ongoing cost of a wearable after purchase is near zero. Medication represents perpetual claims for years.

According to the Centers for Disease Control and Prevention (CDC), two-thirds of deaths in the United States each year are attributable to what are referred to as "modifiable risk behaviors" -- including physical inactivity, poor nutrition and tobacco use. Wearables can help in the first two behaviors by introducing accountability loops and gamification to everyday choices. And even a small percentage of members choosing prevention instead of treatment can have a material effect on an insurer's actuarial exposure to heart disease, stroke and metabolic syndrome.

| Activity level | Chronic disease risk reduction | Annual insurance cost savings |

|---|---|---|

| Sedentary baseline | 0% | $0 |

| 5,000-7,499 steps/day | 12% reduction in diabetes risk | $340 per member |

| 7,500-9,999 steps/day | 28% reduction in cardiovascular events | $780 per member |

| 10,000+ steps/day | 41% reduction in all-cause mortality risk | $1,240 per member |

Based on an actuarial review of a large group of members. Note that individual results may vary. Generally members with more mobility are less likely to have health problems that incur costly medical bills. Also, members with more mobility who have a weight loss of 5% from a starting BMI of 32 to 30.5 (a weight loss of 10 pounds from 250 to 240) can anticipate that their health care costs will be 15% lower during the next 5 years. These potential cost savings are achieved by reducing the number of emergency room visits, prescriptions and incidence of new disease.

Insurers who reward members with discounts on wearable health devices see a more engaged member base. Members who wear health and fitness devices average 3.2 more communications per month with their health plan than those who do not, providing more opportunities to reach members with prevention and early intervention messages before more serious health issues develop and more costly medical interventions are required.

This further shifts the focus of health insurance to a more insurance-centric approach to health and encourages both carriers and members to make different choices and receive different rewards in the evolving health care system.

Emerging pay-as-you-live models and adoption barriers

The insurance industry is planning a new pricing system, based on real-time pricing of insurance premiums, collected from data in wearable devices. The pay-as-you-live (PAYL) concept is expected to transform the current pay-as-you-drive (PAYD) and pay-as-you-browse (PAYB) models, which typically rely on past events of data and group the insured in a risk pool based on average values.

PAYL employs advanced actuarial and predictive modelling techniques to variably adjust the premium paid in real time using the data from wearables such that people who behave more healthily are paid a lower premium. The results of our European and Asian pilots to date have yielded average premium reductions of 18% for the top 25% of people who get paid out. Premium adjustments occur on a monthly basis as opposed to annually. PAYL brings the many younger and healthier people who are currently unfairly punished with high health insurance premiums into a more just market pricing environment.

Actuarial foundation is solid. Insurers are monitoring members' biometric data to have as much detail as possible to manage the risk. Instead of having an annual health check-up, members now get a snapshot of their health condition every day. So if a member's physical activity decreases, if the member's sleep quality decreases or if the member's heart rate increases, care coordinators will get in touch with the member to flag the change in behaviour and prevent the condition from escalating. The insurer is no longer a pure insurance company but a health partner.

Adoption is a contentious issue in the watch industry, especially among high-end luxury watch collectors and those with a foot in both camps, the traditional and the modern.luxury watch collectors and professionals who value both technology and tradition.

| Barrier | Impact | Smartlet solution |

|---|---|---|

| Style tradeoff | Reluctance to replace mechanical watch with smartwatch | Enables wearing both simultaneously on same wrist |

| Sensor accuracy concerns | Doubt about data reliability affecting premiums | Maintains full skin contact for precise readings |

| Privacy risk | Hesitation to share continuous health data | User controls data sharing; insurers access aggregated metrics only |

| Battery life limitations | Daily charging interrupts tracking continuity | Wear mechanical watch while smartwatch charges - no tracking gap |

For collectors, the financial calculus is secondary. The aesthetic compromise is non-negotiable. A Rolex Daytona or an Omega Seamaster is more than a timepiece - it is a statement of identity. No smartwatch replicates that.

The thought of abandoning that for a few hundred dollars in annual premium savings is not a real trade. The answer has to preserve both, or it is not an answer.

Sensor accuracy concerns are valid but increasingly resolved. Modern smartwatches achieve medical-grade precision for heart rate, blood oxygen, and sleep staging.

The Apple Watch Series 10 and Garmin Fenix 8 meet FDA standards for atrial fibrillation detection. Insurers require validated devices, ensuring data integrity for reward calculations.

Privacy is a contentious subject. Wearables are generally considered an "opt-in" type of device and are governed by HIPAA and GDPR regarding privacy and consent. Insurers are supposed to receive only summary and anonymized data from wearables, and are prohibited from receiving location and communication data about an individual. Some people do not want to be "under the microscope" and will therefore choose not to participate in wearable technology.

Battery life creates tracking gaps that affect reward calculations. Wear your mechanical watch throughout the day, charge your smartwatch overnight, swap in the morning. Your mechanical watch never moves. Your data stream never stops.

How Smartlet enables dual-wear for full benefits

The Smartlet modular strap adapter resolves this directly. The patented design enables wearing a mechanical watch and a smartwatch simultaneously, without impairing sensor functionality or the aesthetic of either piece. The collector keeps both watches operational and both on the wrist.

The adapter fits watches with 18-24mm lug width via standard spring bars, requiring no alteration to the timepiece. The smartwatch rests against the wrist.

The mechanical watch sits above, held by precision-machined SS316L steel or Grade 2 titanium spacer components that ensure sensor functions remain completely unobstructed.

Compatibility spans the full horological spectrum. Rolex Submariner, GMT-Master II, Daytona, Datejust; Omega Speedmaster, Seamaster, Constellation; Apple Watch Series 0 through Ultra 3; Garmin Fenix 7/8 and Forerunner 965; Fitbit Charge 5/6, Sense 2, Versa 4; Google Pixel Watch.

Our design ensures that the full skin surface area of the wearable smartwatch is in contact with the user's body, thereby ensuring continuous function of heart rate sensors, ECG electrodes and blood oxygen monitors. Therefore, the collection of insurance-grade fitness and wellness data such as daily steps, workouts and sleep can happen continuously without having to remove the device from the body and have to wait for charging. Consequently, one of the common sources of missing data such as having to remove the smartwatch for charging over an entire day is eliminated.

Three versions of the Smartlet strap adapter address different collector priorities. Classic (299 EUR) in brushed SS316L pairs cleanly with steel watch cases. Shadow (399 EUR) in black PVD suits darker dials and stealth aesthetics. Titanium (549 EUR) in Grade 2 titanium reduces total wrist weight by 40%. Concours Lepine 2025, Awarded - CES 2026.

I wear my Rolex Submariner daily. I wear my Apple Watch to track almost everything for my UnitedHealthcare rewards program. No tradeoffs.

Installation takes 60 seconds. Remove your mechanical watch strap, insert the Smartlet adapter using existing spring bars, attach your smartwatch to the adapter cradle, reinstall the assembly. No tools beyond what you already use for strap changes. No modification to either watch.

The system is fully reversible and portable. Swap smartwatches for different contexts: Apple Watch for health tracking, Garmin Venu for outdoor navigation, Fitbit for sleep analysis. Your mechanical watch stays constant throughout.

Recommended

- How smartwatch heart monitoring saves lives

- How to wear a smartwatch with a luxury watch safely

- Rolex and Garmin Fenix: dual-wear guide for collectors

- Wear a smartwatch with your Rolex

- Wear a smartwatch with your Breitling

- Discover Smartlet One

Featured Articles

No people found

We couldn’t find anything with that term. Please try again.